Investment Management Newsletter - Q1 2025

The Quiet Before the Storm

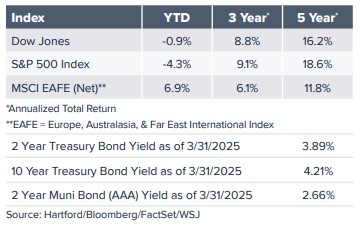

The first quarter of 2025 ended in a muted fashion as market participants grew concerned about upcoming tariff implications (inflation and slower growth) and job losses resulting from the Department of Government Efficiency (DOGE) initiatives. Equities and asset classes that rose dramatically after the election came back to near-election levels. The S&P 500 fell 4.3%, led lower by the Magnificent Seven (Mag-7) group of stocks that led the markets during 2024. The artificial intelligence theme that drove the Mag-7 companies higher was rocked in the quarter by the “DeepSeek Moment”, when a Chinese generative artificial intelligence program was able to produce results similar to those of the U.S. programs at a fraction of the cost.

The general weakness cascaded through riskier asset classes as the S&P 400 Midcap Index fell 6.1% during the quarter and the S&P SmallCap 600 Index fell 8.9%. International equities, on the other hand, trended higher thanks to a weaker U.S. dollar and continued stimulus by foreign central banks. Developed International equities, as measured by the MSCI EAFE Index, rose 6.9% during the quarter and Emerging Market equities, as measured by the MSCI Emerging Markets Index, rose 2.9%.

Fixed Income

Bonds were able to partially offset weakness in the equity markets during the quarter as investors sought to reduce risk in their portfolios. The Bloomberg Intermediate Aggregate Bond Index rose by 2.4% during the first quarter. High-yield bonds rose as well but not as much as higher rated corporate and Treasury bonds. The first quarter saw 10-year Treasury Bond yields drop from 4.58% to 4.21%.

Alternative Assets

While equity markets zigged lower, alternatives zagged higher. Commodities rose 8.9%, helped significantly by gold, which rose 18.2% during the quarter. Infrastructure investments rose mid-single digits helped out by Master Limited Partnerships. Publicly traded Real Estate Investment Trusts were also higher by mid-single digits. Finally, absolute return strategies were higher by 1.1% as measured by the HFRX Absolute Return Index.

Tariffs and the Threat Thereof

President Trump announced new tariffs on “Liberation Day.” These were tariffs of 10% on all imported goods taking effect on April 5, followed by additional tariffs on individual countries. Our two largest trading partners, Canada and Mexico, were largely exempt from this round of tariffs. The administration announced reciprocal tariffs ranging anywhere from 17% (Israel) to 49% (Cambodia). We note the term “reciprocal tariffs” is arguably a misnomer, because the country-specific tariffs imposed by the U.S. were calculated on factors well beyond a simple reflection of tariffs other countries impose on U.S. imports. The threats of slowing economic growth and higher prices took their toll on the equity markets after the tariff announcement, including back-to-back 5% drops on April 1 and 2. The market drop resulted from reduced corporate earnings forecasts due to expectations of lower profit margins and sales volume. Margins are pressured when a company cannot pass on the full impact of tariffs to their customers, and rising prices can affect sales volume. As market participants analyzed the projected impacts of the announced tariffs, market indices came down rapidly.

The back-to-back drop was the sixth worst two-day drop in U.S. equities since 1940. Across the previous five worst two-day drops, the average returns for one month, three months, six months and one year into the future were all positive. The six-month and one-year average returns were 15.8% and 32.6%, respectively. Another way to describe the extreme movements and panic is to look at the volatility index (VIX). The VIX measures expected volatility based on pricing of near-term options on the S&P 500. The VIX closed the week ending April 4 at nearly three times its normal level at 57.78. Since 1998, there have been eight instances of the VIX closing above 40. They include COVID, the U.S. debt downgrade, the “Flash Crash” and the Great Financial Crisis. In six of eight cases, the S&P 500 return was a double-digit percentage one year later. Three years and five years later, the S&P 500 was higher in all cases.

As of this writing, President Trump paused all tariffs except the 10% baseline tariff and tariffs on China. The VIX has now fallen below 40, and the U.S. equities markets continue to fluctuate.

Where Does Monetary Policy Fit?

Federal Reserve Chairman Powell and the rate-setting committee now find themselves backed into a corner. With the 10% baseline tariffs in place and punitively high tariffs on China, inflation will likely remain elevated until a long-term solution is found. This will prevent the Fed from cutting short-term rates aggressively. Economic growth and employment will likely deteriorate, which will keep the Fed from increasing short-term rates aggressively. Powell and other Fed Governors have said, even after Liberation Day, that they would like to understand the eventual effects of the outstanding tariffs before they alter monetary policy. Economists’ and analysts’ estimates for the Fed’s overnight interest rate currently vary more widely relative to historical norms.

Why Broadway?

Broadway’s investment philosophy has always been to buy high financial quality assets that perform better in down markets while participating strongly in up markets. Our discipline has proven itself during every protracted market downturn in memory. As we are witnessing now, today’s current challenging market conditions are vindicating our strategies once again.

During these challenging times, Broadway’s portfolio managers are looking to contain risk and take advantage of any opportunities that arise in fluctuating markets through asset selection, tactical changes and timely rebalancing of portfolios.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].