Investment Management Newsletter – 1st Quarter 2026

The War…What Is It Good For?

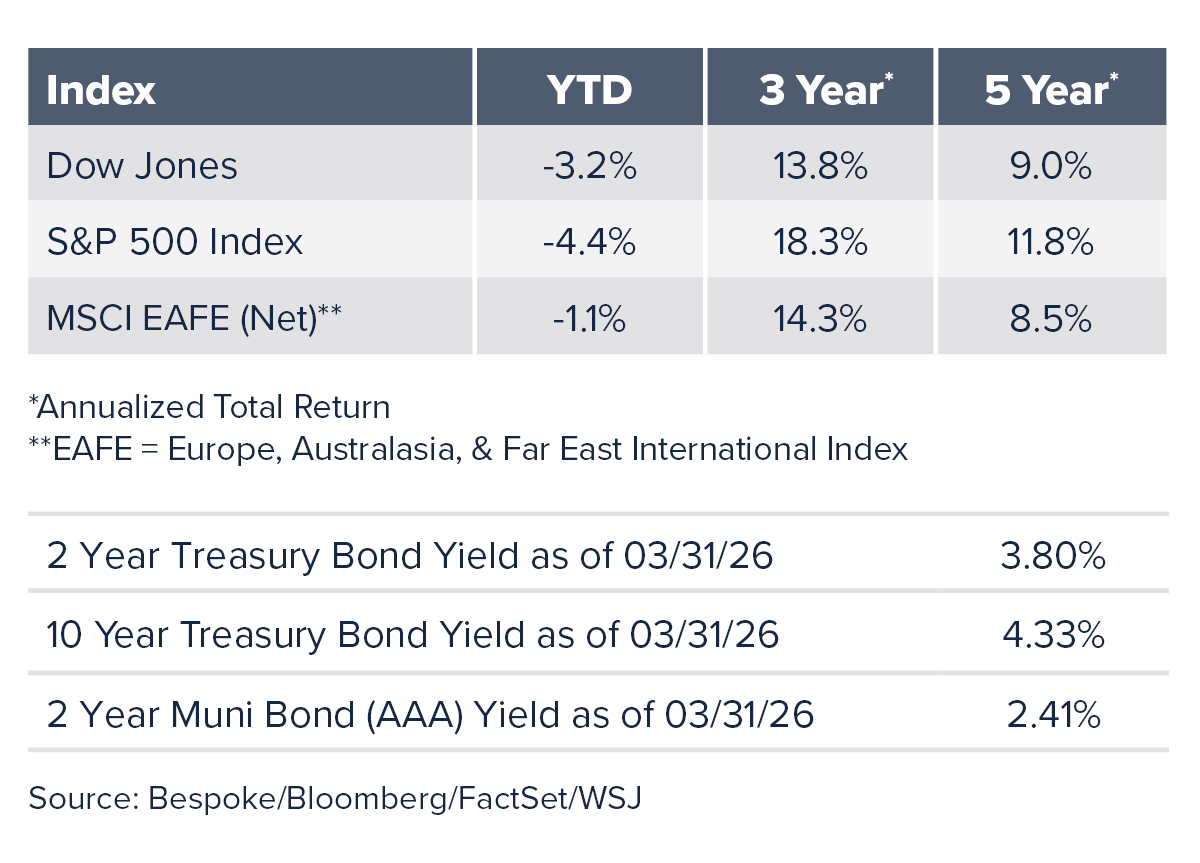

The markets continued their march higher from late 2025 for the first half of the quarter until software companies traded lower on AI replication fears. Markets steadily moved sideways through February until the beginning of the Iran War when markets saw some of their worst returns since last year’s reciprocal tariff rollouts. The S&P 500 ended the quarter down 4.4% with the tech-heavy NASDAQ Composite falling almost 7.0%. In contrast, mid-cap stocks rose 2.5% and small-cap stocks gained 3.6% likely benefiting from less exposure to the Middle East. International stocks reversed earlier gains during the first two months of the year as the U.S. dollar significantly strengthened following the initial strikes of the Iran War. Value stocks outperformed growth stocks by almost 12.0% as investors sought safety. The Russell 1000 Value Index gained 2.1% during the first quarter.

While previous international conflicts have had small, short-lived impacts on the markets overall, the current situation presents more complex and far-reaching consequences due to its effect on the global energy supply. To try and determine where markets are headed, it helps to compare previous geopolitical events to the Iran War, namely the Suez Crisis, the Arab Oil Embargo, the Iranian Revolution, and the Gulf War of 1990-1991. Traffic through the Strait of Hormuz has all but stopped, which is significant as 20% of the 100-million-barrels-per-day oil market flows through this chokepoint. While some production is being rerouted through alternate pipelines, analysts believe at least 10 million barrels are being held back as certain energy-producing assets were bombed. This disruption had a bigger supply impact than any of the four previously mentioned conflicts. Complicating matters, spare capacity from Saudi Arabia and other major exporters in the region cannot be ramped up while the Strait of Hormuz is effectively shut. Global oil futures have risen over 80% since the beginning of the year as of the time of this writing. Oil prices saw less of an increase during the Russian invasion of Ukraine, but prices were higher going into that conflict, and major disruptions to oil supply never quite materialized as expected. Because the recent path of oil prices has been very similar to that of the Gulf War, it makes for a better comparison than the Ukraine invasion. The S&P 500 is down 5.3% from 9 days before the bombing of Iran began. The S&P 500 was down over 10% at this same point in the Gulf War and had been more volatile during its journey to the lower lows. The market had recovered most of its losses by this point during the Ukrainian invasion and had not fallen as far during the Arab Oil Embargo.

Typically, during times of geopolitical stress and uncertainty, global investors flock to the safety of U.S. Treasury bonds as the ultimate safe-haven investment. That did not occur in this instance as the 10-year yield jumped 0.5% since the beginning of the Iran War. Rates followed a similar path and magnitude at this point during both the Ukraine War and Gulf War. Rates rose quicker during the Gulf War; however, the U.S. was not energy-independent during that energy crisis. Rates have climbed due to several factors driven by the Iran War. First, higher global oil prices increase the prices of the many items that have petroleum products as a major input. Second, transportation costs will rise due to an increase in fuel prices for planes, ships, trucks, and electricity production. Companies, including many airlines and even Amazon logistics, have begun passing these increases onto customers in the form of surcharges. As diesel and gasoline prices rise, consumers around the globe will inevitably cut back on their spending. Prices will decrease once oil cargo ships can pass through the Strait of Hormuz again, but the drop may not be as dramatic as many export facilities have been damaged and could take months or years to be repaired. After the largest-ever release of crude by the International Energy Agency, including 172 million barrels from the U.S., many resources to buffer price shocks have been used. A large share of urea used for fertilizer is also exported through the Strait of Hormuz, which will increase fertilizer prices for farmers and, therefore, food prices for consumers. To mute the inflationary impacts of higher energy and fertilizer prices, the sooner the Iran War ends, the sooner goods prices will stop accelerating.

Rates And The Fed

Fixed income total returns were essentially flat during the quarter as interest rates rose post-Iran War after having dropped during the first two months of the year. The 10-year yield ended the quarter at 4.33% after starting the year at 4.17%. As the year started, consensus expectations called for the Fed Funds rate to decrease by at least half a percent with cuts likely in the middle and end of the year. With the Iran War, the cut predictions have now been wiped away and at one point the Fed Funds futures were pricing a rate hike in 2026. Higher oil prices do not impact the core measures of inflation the Fed watches; however, there will likely be some creep in consumer prices overall. Complicating their efforts, the labor market has been particularly weak with job additions being anemic from AI-related efficiencies and the effects of last year’s DOGE cuts. Historically, this would have led to an increase in the unemployment rate, slower spending, and a risk of recession; however, none of these have occurred because labor supply has not increased as net immigration has substantially decreased. The Fed remains “data-dependent” as a variety of competing forces keep it in a neutral stance.

A Note on Private Credit Funds

As AI showed it could replicate many features of the Software as a Service (SaaS) industry, not only did it impact publicly traded companies, but it also spread fear that companies owned by private equity funds that issued lots of debt would be imperiled. Private Credit Funds, usually in the form of Business Development Companies, hold most of this debt. In fact, software company debt comprises about 20% of these funds on average. Due to the structure of these funds, investors are usually only entitled to redeem an aggregate of 5% of the fund every quarter. This is not an issue unless many investors want out at the same time, which is what is occurring at the moment. Now, many funds have capped redemptions at 5%, forcing investors to request amounts more than they really want to redeem under the assumption that they will only receive a fraction of what they requested each quarter from the funds. Broadway Wealth Management has always considered liquidity of our investors’ assets of utmost importance given the risk of certain asset classes having their liquidity impaired. Generally, all of Broadway Wealth Management’s financial assets can be converted to cash equivalents in one trading day. To reiterate, Broadway Wealth Management currently has no direct exposure to private credit funds.

Alternative Assets

It should be no surprise that crude oil was the winner in alternative assets with a first quarter gain of over 72.0% for West Texas Intermediate oil. This movement drove pipeline and infrastructure assets higher during the quarter with the MSCI World Core Infrastructure Index up 7.8%. Within the commodity bull market, gold increased over 7.1% and its far more volatile counterpart, silver, rose more than gold. Real Estate Investment Trusts also had a positive quarter, gaining 3.8%. The HFRX Absolute Return Index was up 0.9%. These returns again show the importance of having liquid alternative assets as part of a diversified portfolio during volatile and uncertain times.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].