Investment Management Newsletter – 2nd Quarter 2025

Rebound for the Record Books

The second quarter of 2025 was one for the record books as U.S. stocks hit their trading year lows in the aftermath of President Trump’s “Liberation Day” tariffs, which were higher than expected. In the two days following the announcement, the S&P 500 tumbled over 10% for only the fourth time since World War II (Ned Davis Research). At the height of tariff panic, the stock index was down 15.3% on a year-to-date basis and 18.9% from its all-time high on February 19.

As remarkable as the decline was, the rebound was even more historic. After shrugging off the initial damage to the markets, the president declared it was a “GREAT TIME TO BUY” in a social media post on April 9 and subsequently announced a 90-day pause on many of the planned tariffs, sending the S&P 500 soaring 9.5% for its best day since the financial crisis in 2008. The market enjoyed a strong second half of April and then roared higher in May to close approximately in line with year-opening levels. By the end of June, stocks had rebounded just under 25% to new highs, meeting the threshold for a new bull market of at least 20%. According to Dow Jones Market Data, starting at the February highs, this rebound was the fastest recovery on record from a 15% drop back to an all-time high. The large and rapid movements experienced in the second quarter serve as an important reminder that to have a successful investment experience, investors should focus on time in the market rather than trying to time the market. Missing a handful of the best days can significantly reduce returns.

Expect tariff concerns to resurface before the newly established August 1 deadline. Unlike the second quarter, we expect the markets to have better adapted to surprises on this subject and therefore do not expect as much volatility as was seen in April. As always, we take these possible scenarios into account when making long-term allocation decisions and look for opportune investments when given the chance.

Mean Reversion vs. First Quarter

Although most asset classes posted gains in the second quarter, leadership among sectors, investment styles and geographies were virtually opposite of what we saw in the first quarter.

U.S. Equities

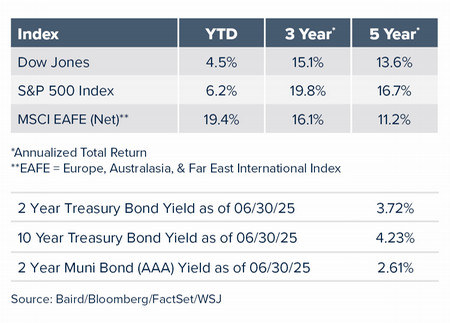

On a total return basis, the S&P 500 rose 10.9% for the quarter and was higher by 6.2% year-to-date. Looking under the hood, growth stocks soared while value stocks lagged, reversing the first quarter’s trend of value stock leadership. The biggest story of the quarter was the rally in the Information Technology sector, which climbed 23.7% after falling 12.7% in the first three months of the year. Likewise, Communication Services stocks rose 18.5% after falling 6.2% in the first quarter, while Consumer Discretionary stocks gained 11.5% after losing 13.8% to begin the year. The Industrials sector rallied 12.9% after a 0.2% loss in the first quarter, cementing it as the best performer year-to-date. On the other side of the spectrum were Healthcare and Energy stocks, which declined after posting solid gains in the first quarter. Outside of large-cap, mid-cap (+7.9%) and small-cap (+8.5%) stocks each posted solid gains after losses of 3.4% and 9.5%, respectively, in the first quarter. The performance of smaller businesses lagged their larger-cap counterparts due to their sensitivity to higher interest rates and potential margin pressure from tariffs.

International Equities

Non-U.S. stocks continued their strong performance into the second quarter as developed international stocks rose 12.0% (MSCI EAFE) and emerging market stocks gained 12.2% (MSCI EM). A decline in the value of the U.S. dollar versus other currencies boosted international returns in dollar terms. The U.S. dollar index plunged 10.8% through June, its worst first half since 1979. Much of the slump came in April after the tariff news, but unlike other asset classes the dollar did not rebound as concerns surfaced about the budget deficit and the dollar’s viability as a reserve currency.

Fixed Income

Bonds posted respectable returns in the second quarter, despite elevated volatility that sent longer-term yields soaring as investors digested fresh concerns about the federal debt and a declining appetite for U.S. Treasury bonds. The yield on the 10-year Treasury note ended the quarter at 4.23% after climbing as high as 4.60% and falling to a low near 4.00% during the quarter amid the tariff roll out, the tax bill debate and Middle East conflict. The Bloomberg U.S. Intermediate Government/Credit Index, a broad measure of high-quality bonds, rose 1.7% for the quarter.

Alternative Assets

Reversing course from last quarter, broad commodities declined 3.1%, primarily due to an 8.9% drop in crude oil prices, despite geopolitical tensions ramping up in the Middle East in June. Gold continued to climb in the second quarter, although the 5.9% gain was more muted compared with an 18.2% rise in the first quarter. Global infrastructure investments gained 4.5% on continued flows to data center and energy transition projects. Real Estate Investment Trusts fell 0.9%, as a lack of clarity on interest rate and trade policy weighed on the sector. Finally, absolute return strategies were higher by 1.3% as measured by the HFRX Absolute Return Index.

Federal Reserve Remains on Hold

The U.S. economy, as measured by real GDP, contracted by 0.5% in the first quarter, primarily due to a surge in imports as businesses built up inventories in anticipation of tariff increases. Although a rebound is expected in the second quarter, the growth trajectory for the second half is anticipated to be slower than in previous years as tariffs filter through the economy. The Atlanta Fed’s GDPNow model currently estimates growth of 2.6% for the second quarter. At its June meeting, the Federal Reserve held the fed funds rate steady in the range of 4.25% - 4.5% as expected.

Although economic activity continued to expand at a solid pace and unemployment remained low, inflation remained somewhat elevated. With no change in rates, all eyes were on the Fed’s Summary of Economic Projections for clues about the path forward. This quarter’s projections were stagflationary (i.e., rising inflation combined with slow economic growth and rising unemployment), revising its growth forecast downward for 2025 (1.4% GDP), and forecasts for inflation (3.0% PCE) and unemployment rate (4.5%) upward for year end. The committee’s outlook for interest rate policy (the dot plot) suggested we might see two rate cuts for the second half of 2025, but only one cut for 2026.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].