Market Insights: Investment Management Q3 2024

What Comes Around Goes Around

It seems like every market commentary since the beginning of 2023 could not avoid discussing the dominance of a handful of Large Cap technology stocks often referred to as the “Magnificent Seven.” The stellar returns for these seven stocks were largely a function of their investment in and market leadership of the nascent artificial intelligence (AI) phenomenon. The combined returns of the “Mag 7” have undoubtedly been magnificent, producing a 76% return in 2023 vs. 26% for the S&P 500 index. But 2024 has shown signs of slowing for the Mag 7, with a combined return of 35% vs 22% for the S&P 500. Investors are starting to doubt that the massive investments required for AI data centers will produce the requisite returns.

Fortunately for investors, a different theme stood ready to drive the market direction–falling interest rates. Lower rates allowed the market to broaden from the Mag 7 to the other 493 stocks in the S&P and beyond. Virtually every market segment found falling rates to be an attractive dance partner. Smaller companies, in particular, respond favorably to lower rates given that 30% of Russell 2000 (the small cap index) debt is floating rate compared with 6% for the S&P 500. This broadening of market returns was a prerequisite for a healthy, more stable, bull market with room to run.

Widespread Strength

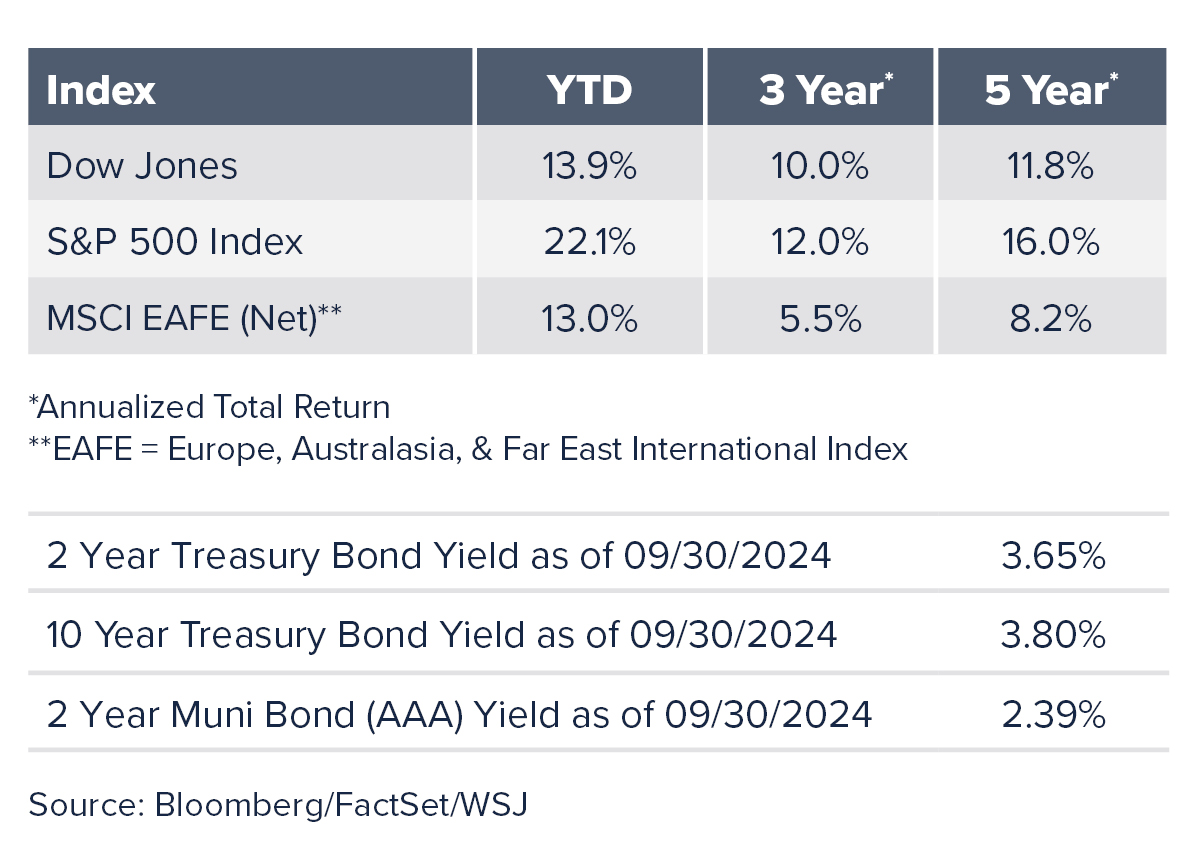

The S&P 500 added 5.9% in the third quarter, bringing its year-to-date return to 22.1%. Returns through the first nine months for the U.S. stock market are the highest for the 21st century. Looking deeper into the details, the Consumer Discretionary, Financial Services, Industrials, Real Estate and Utilities sectors all posted double digit returns in the quarter. The only sector posting a loss in the third quarter was Energy, likely due to the slowdown from China and looming supply increases from OPEC at the end of this year.

It is unsurprising that the dollar weakened 4.8% against a basket of currencies during the third quarter as U.S. interest rates fell. This helped overseas stocks boost returns when translated back into U.S. dollars. International stocks rallied with the MSCI EAFE Index jumping 7.3% during the quarter and the MSCI Emerging Markets index up 8.8%. Elsewhere, the S&P Midcap 400 and S&P SmallCap 600 ended the quarter up 6.9% and 10.1%, respectively. On a year-to-date basis, mid caps were up 13.5% and small caps were up 9.3%. Factors contributing to the strong equity performance this year include the Fed entering an easing cycle, a broadening of the market, and the slide in energy prices.

Considering valuations, the forward P/E ratio of the S&P 500 now sits at 20x. While higher than average, valuations remained well within the normal range of 13-24 times forward earnings. Robust earnings growth of 11.3% reported in the quarter was the highest since 2021, justifying these valuations.

When looking back over the last 40 years of S&P 500 quarterly performance, the fourth quarter has on average, significantly outperformed the first three quarters of the year. Average performance in the first, second and third quarters has been 2.3%, 2.9%, and 0.4%, respectively. The fourth quarter has produced an average return of 4.8%. With elections having occurred in half of all those fourth quarters, history has demonstrated the journey toward above average returns is seldom smooth.

Alternative Assets

Alternatives with lower correlations to traditional stocks and bonds may limit the upside during strong bull markets but are often effective diversifiers during market volatility. Hedge funds have returned 1.2% in the third quarter and 4.0% (HFRX Absolute Return Index). Gold was up 28.0% year-to-date with half of that gain in the third quarter alone as gold hit a record high of $2,685 per ounce near quarter end. Falling interest rates and Asian central bank buying pushed gold higher. Oil fell 16.0% in the quarter with West Texas Intermediate crude finishing marginally down from the beginning of the year price to $68 a barrel. The effects of escalating tensions in the Middle East were offset by the Chinese economic slowdown.

Bond Rates Headed Down

The 10-year Treasury yield ended the third quarter at 3.80%, significantly lower than it was at its peak of 4.70% for the year occurring on April 25th. The 2-year moved dramatically as well falling in the quarter from 4.49% to end at 3.65%. The drop in yields caused the Bloomberg U.S. Aggregate Index to jump 5.2% during the third quarter. The inverted yield curve finally corrected to a normal positively sloping curve with 10- year yields pushing above 2-year yields in the quarter. The yield curve had been inverted since 2022. Riskier credit as measured by the Bloomberg U.S. Corporate High Yield Index was up 5.3% during the quarter in a sign that the risk of recession has abated.

The Long-Awaited Fed Pivot

The Fed expressed confidence that inflationary pressures have been curbed enough to shift its focus from maintaining price stability to the other side of its dual mandate–maintaining full employment. The Fed’s main inflation indicator, the core-personal consumption expenditures (PCE) index, has declined from its postCovid peak of 5.6% to 2.7%, within reach of the 2.0% goal. Unemployment has been on a slow climb from its low of 3.4% in April 2023 to 4.2% as of quarter-end. This level is still considered low by historical standards. The higher interest rates of the last few years are now a risk to unemployment continuing to climb. With two more Fed meetings remaining in 2024, both are likely to produce more rate cuts. As always, the Fed’s caveat is that decisions will be dependent on incoming economic data.

While the Fed does not have a specific target for full employment, many economists believe a rate of 3% to 5% is normal and not restrictive to a growing economy. Fed Chair Jay Powell explained the balance the Fed is trying to achieve lies between waiting too long to cut rates at the cost of economic activity and employment, and cutting too quickly, undoing much of what they have already accomplished to reduce inflation and having to start over.

With that background, the Federal Reserve pivoted to easing financial conditions by cutting the Fed Funds rate 0.50% at their September meeting. The market was unsure if the cut would be 0.25% or 0.50% and the market was pleasantly surprised by the aggressive move. Following the Fed cut, bond markets rallied, pushing yields down. Many homebuyers have also been on the sidelines waiting for mortgage rates to fall. Whether lower mortgage rates will lead to increased demand or if higher prices and low relative inventory continue to hamper demand is uncertain.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].