Investment Management Newsletter – 3rd Quarter 2025

Law of Inertia

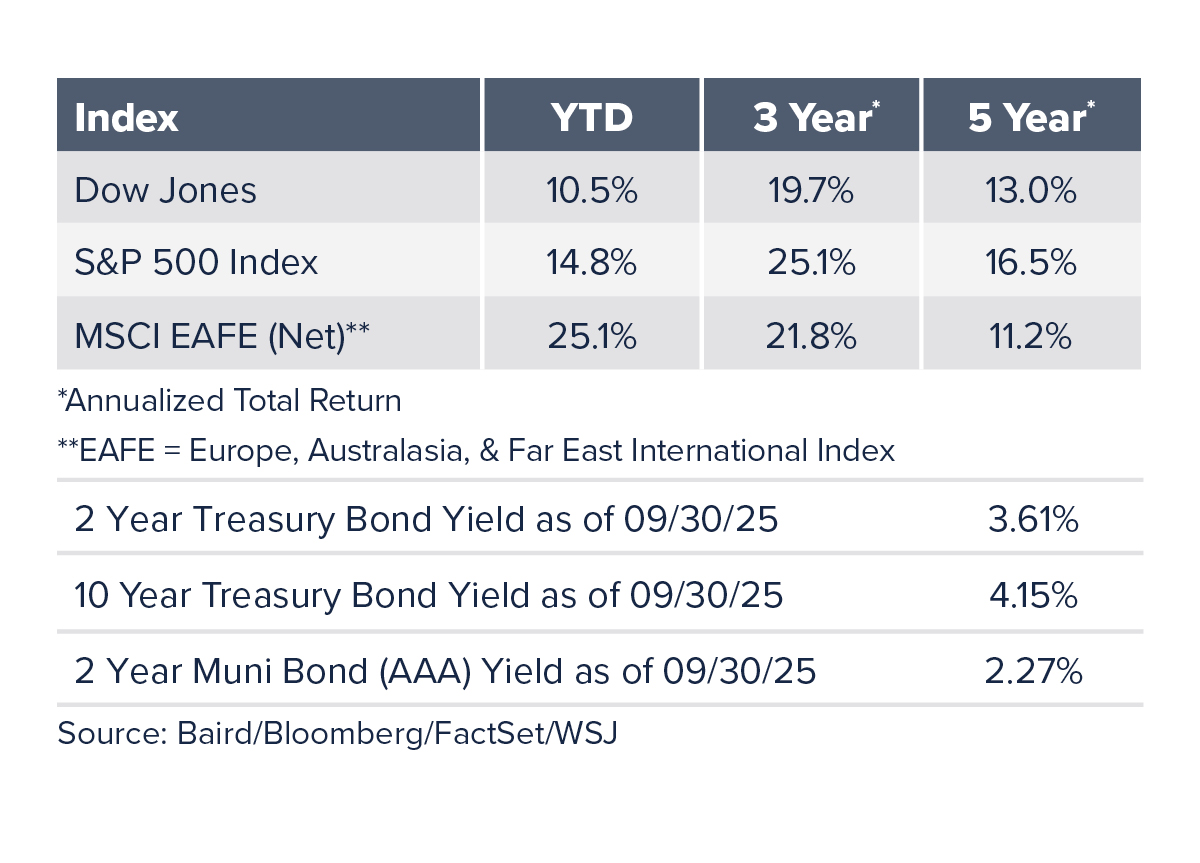

Equity markets maintained their momentum and extended their rally throughout the third quarter. Despite tariff uncertainty, persistent inflation worries, and concerning jobs data–factors that would typically slow a rally–the S&P 500 set new all-time highs on 23 days this quarter, or more than once every three trading days.

Tariff policy this year has been akin to a broken traffic light, changing unpredictably between green, red, and yellow until being declared a traffic hazard. The green light occurred as tariffs were announced back in April, followed shortly by the red light, a 90-day pause, which was extended to August. Before the pause expired, a framework for a trade deal with the European Union including reduced tariffs was announced, analogous to a flashing yellow light, as tariff implementation would proceed, but at a more measured pace. Then, a ruling from the U.S. Court of Appeals found President Trump overstepped his authority by imposing sweeping tariffs under an emergency powers law. Trump will likely appeal to the Supreme Court, and a final decision could take months.

Concerns about the strength of the labor market were highlighted when non-farm payroll data showed a downward revision of 911,000 jobs from initial estimates, the largest since 2002. This added to mounting evidence of a weakening U.S. job market. Perhaps more surprising than the revision itself was the political fallout: President Trump cited the revision as evidence that the Bureau of Labor Statistics (BLS) was broken and dismissed the BLS Commissioner, seeking to replace her as a move to restore trust and confidence in the data.

Looking forward to the fourth quarter, investors have history on their side. Historically, the fourth quarter has outperformed the first three quarters and has delivered positive returns in over 80% of years since 1980. Still, before we get too far ahead of ourselves, one issue may dominate the headlines in the coming days.

A Government Shutdown

At the time of this writing, Congress has been unable to generate the supermajority of 60 votes in the Senate to pass an appropriations bill or continuing resolution. As a result, non-essential federal workers have been furloughed, and certain government services have ceased. If this feels familiar, it’s because it is. The U.S. government has had a total of 21 previous shutdowns, with an average duration of less than eight days. Most shutdowns get resolved quickly, but the most recent one in 2018 was the longest on record at 34 days. Historically, markets tend to look past shutdowns, which rarely have a lasting impact on a diversified investment plan. However, a prolonged shutdown could delay key economic reports, such as monthly employment, inflation, and trade data, reducing visibility of the economy’s condition.

Small-Cap Comeback

On a total return basis, the S&P 500 delivered a strong 8.1% return in the third quarter, bringing the year-to-date return up to 14.8%. Small-cap stocks staged a notable rebound, with both small value and small growth indices returning over 12% for the quarter. The artificial intelligence theme remained strong, powering the Information Technology sector to a return of 13.2%. Communication Services rose 12.0%, and Consumer Discretionary gained 9.5%.

Returns were broad-based, with only one sector having a negative quarterly return. Consumer Staples declined 2.4%. Even with the third quarter decline for Consumer Staples, every sector now has a positive year-to-date return heading into the year’s final quarter. Healthcare currently has the lowest year-to-date return of any sector at 2.6%, while on the other end, Communication Services leads with a return of 24.5% followed closely by Information Technology at 22.3%.

U.S. Dollar Stabilization

After declining more than 10% in the first half of the year, the U.S. dollar appears to have found a floor. The U.S. Dollar Index rebounded slightly, rising 0.9% in the third quarter. Despite the stronger dollar, non-U.S. stocks continued to outperform. Developed international markets (MSCI EAFE) rose 4.9% while emerging markets (MSCI EM) gained 10.9%. This continued success for international markets has led to a stellar year-to-date return of 25.1% for developed markets and 28.2% for emerging markets.

Fixed Income

While equities captured most of the spotlight, bond yields quietly trended lower. The yield on the 10-year Treasury ended the quarter at 4.15% after climbing to nearly 4.50% in July and bouncing off the yearly low of 4.00%. The Bloomberg U.S. Intermediate Government/Credit Index, a broad measure of high-quality bonds, rose 1.5% for the quarter.

Gold Still Shining

Broad commodities, as measured by the Bloomberg Commodity Index, increased 3.7% in the third quarter, with gold contributing significantly. Gold added 16.1% this quarter, outperforming most equity benchmarks and bringing its year-to-date return to an impressive 45.4%. Real Estate Investment Trusts also gained 2.7%, as markets gained clarity regarding the future path of interest rates.

Fed Funds Rate Outlook

The U.S. economy, as measured by real GDP, grew at a 3.8% annualized rate in the second quarter. This might be overstated due to shifting tariff policy, but is a positive signal of economic momentum. As expected, the Federal Reserve lowered the Fed Funds rate by 0.25% to a range of 4.00% - 4.25% in the September meeting, marking the first cut of the year and the first since December 2024. Despite inflation remaining “somewhat elevated,” Chair Jerome Powell described the cut as a risk-management tool aimed at balancing the Fed’s dual mandate: price stability and maximum employment. A notable dissent in the form of a vote for a 0.50% cut came from Stephen Miran, recently appointed by the President to replace resigning Fed Governor Adriana Kugler. Currently, markets are pricing in two more 0.25% rate cuts by year-end and another two in 2026. That outlook could shift if President Trump is able to appoint others to the Fed who are more aligned with his views on where interest rates should be.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].