Investment Management Newsletter – 4th Quarter 2025

The Same but Different This Time

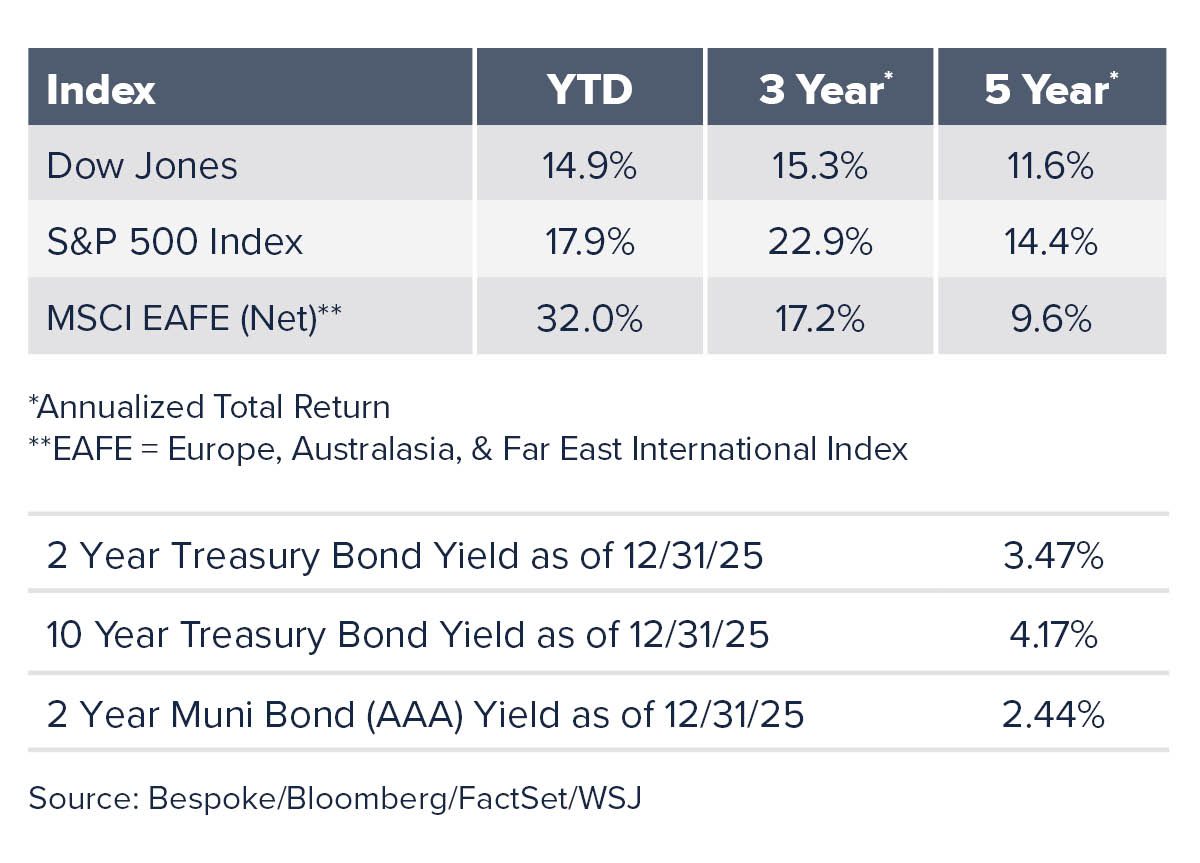

After hitting 46 all-time highs during the year, the S&P 500 finished 2025 with a total return of 17.9%. That followed 2023, when the index rose 26.3%, and 2024, when it gained 25.0%. Three consecutive years of double-digit returns from the S&P 500 have occurred only three other times since the index was created in 1957. Given that previous bull markets have averaged four to five years, there may still be room for this bull to run.

This market has undoubtedly been powered by the massive technological innovation of Artificial Intelligence (AI). As years pass, the question of “Will AI make a difference?” has now become “What can’t AI impact?” Data centers that are larger than football fields and packed with $50,000 semiconductor chips seem to be popping up everywhere. The energy needed to cool these facilities has rapidly outpaced grid operators’ ability to provide power, forcing some data center operators to secure their own power. Even a lack of water for cooling has become a limiting factor.

But there was far more to 2025 than the AI juggernaut. Tariffs dominated the headlines, along with multiple wars in the Middle East, massive government layoffs, the longest government shutdown in history, and more interest rate easing by the Fed. The start of the global trade wars with tariffs in April led to a bear market, where the stock market dropped to an intraday low that was 20% below its February peak. The suspension of most tariffs a week later propelled the market 9.5% higher in a day on April 9th. That rally largely continued through year-end with a slow grind higher.

The stock market has never been more concentrated, with the top ten stocks accounting for 42% of the S&P 500 market value. Such high concentrations tend to increase volatility of an index by decreasing its diversity.

While all 11 S&P 500 industry sectors generated positive returns last year, Communication Services and Information Technology are the two sectors that performed the best, up 33.6% and 24.0%, respectively. The concentration of growth-oriented names in those sectors, often referred to as the Magnificent 7, is one reason growth stocks outperformed value stocks again in 2025, by about 3%. A broadening market and other stocks gaining strength could be supportive of positive returns for 2026.

Small- and mid-cap indices value exposure, along with their lack of participation in the AI trade, were some of the reasons they lagged large caps in 2025. Mid-cap stocks returned 7.5% for the year, with small-caps trailing at 6.0% based on the return of the S&P 600. Both indices followed large caps down by close to 20% in early April before rallying through year-end. Lower interest rates tend to favor smaller companies because they are more dependent on borrowing from banks, versus larger companies that can access the capital markets.

International Returns Impressed

Non-US stocks had a banner year given the softening of the US dollar. The dollar’s 9% depreciation during 2025 enhanced the returns of foreign stocks by a commensurate amount, leaving developed international equity net returns at 32.0% and emerging market equity returns at 34.3% for the year. The last time international stocks bested their US counterparts was in 2022. The 14.5% margin of outperformance over US stocks was the largest in the past 15 years.

Monetary Policy and Bonds

The Federal Reserve continued to ease rates and cut the overnight rate three times during 2025 by a total of 0.75%, leaving the Federal Funds rate range at 3.50 - 3.75%. The Federal Open Market Committee anticipates one or two more quarter-point cuts for 2026.

With the yield on the 2-year US Treasury falling during the year from 4.22% to 3.47% and the 10-year yield falling by 0.36% to 4.17%, the yield curve steepened during 2025. As a result, taxable and municipal bonds generated mid-to-high single-digit returns for the year. The nearly 7.5% return for the Bloomberg US Aggregate Bond Index was its highest return since 2020. The high-yield market, which tends to move more in line with equities, produced some of the highest returns within fixed income, with an 8.6% return for the Bloomberg US Corporate High Yield Index.

Alternative Assets

Based on the return for the S&P GSCI Gold Index, gold was up an astounding 64.4% in 2025, thanks to its attractiveness in an environment of geopolitical uncertainty, lower interest rates, and the unease over US debt levels having tripled since 2007. Meanwhile, the HFRX Index of hedge funds was up 7.1% for the year.

The Economic Backdrop

The strong stock market returns for the year occurred in an economic environment marked by solid GDP growth, rising unemployment (up 0.6% year-over-year to 4.6% as of November 2025), and stubborn inflation at 2.8% year-over-year. Inflation remains above the Fed’s 2% target. The consensus for economic growth this year, roughly 2.5%, is expected to be powered by continued fiscal stimulus, which should provide a tailwind for stocks.

What Lies Ahead for 2026?

Major risks for the stock market in 2026 include the possibility of an AI bubble correction. The determination of whether AI could be in a bubble is a topic of frequent debate. An argument against the bubble thesis is the tremendous earnings and earnings growth of the large-cap technology stocks that are leading the AI revolution. Another risk for 2026 could be that sticky inflation causes the Fed to change course and raise interest rates. Also, the weaker labor market with unemployment now up to 4.6% could tilt the economy into recession. Finally, valuation (as measured by the Forward Price/Earnings ratio for the S&P 500 of 26x) is about 30% higher than the 30-year average. Supporting this high valuation are expected earnings growth of 8.3% for calendar year 2025 and an eye-popping 15.0% expected in 2026. Broadway Bank’s experienced, highly credentialed Wealth Management team continues to rigorously analyze each security that goes into client portfolios with a strong emphasis on risk management.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].