S&P 500 Performance and Market Insights 2024

Bull Markets and Big Gains in 2024

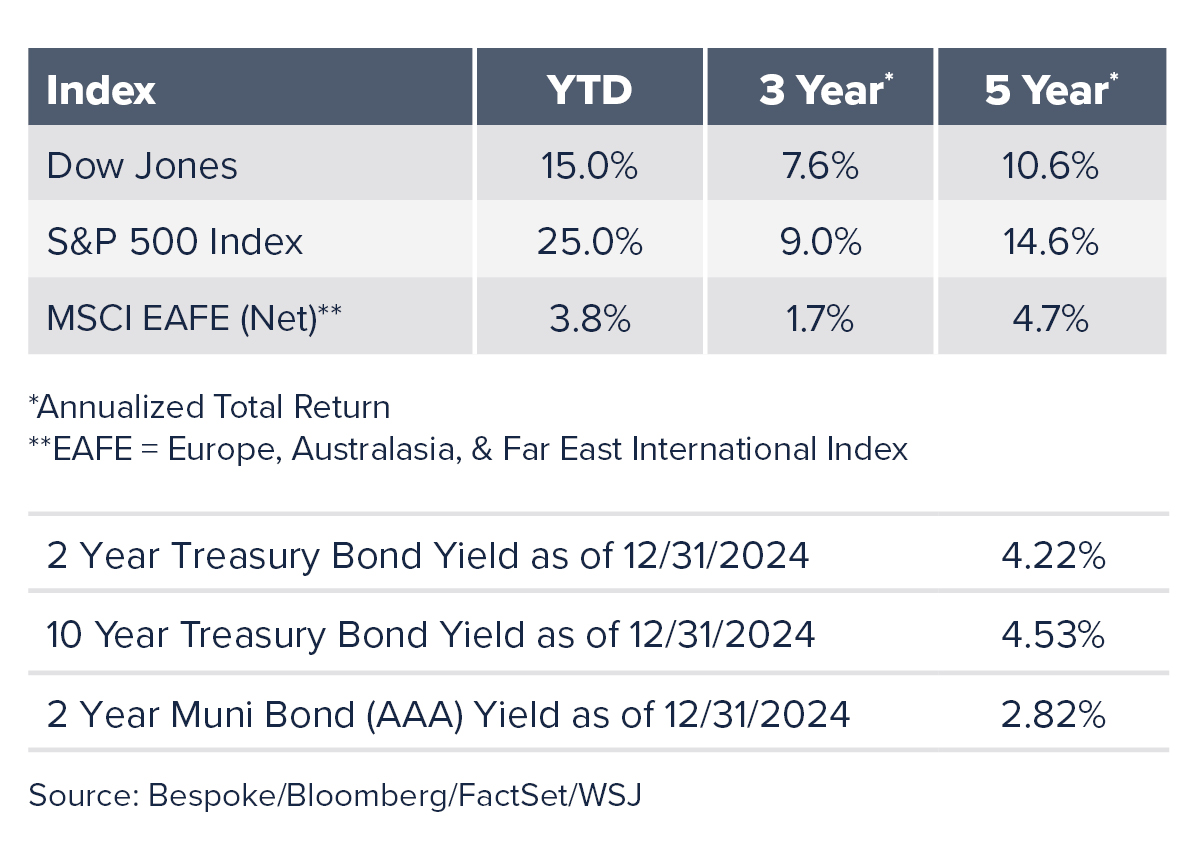

After hitting 57 all-time highs during the year, the S&P 500 finished 2024 with a total return of 25.0%. That followed another far above-average year in 2023 when the index rose 26.3%. Two consecutive years of returns exceeding 20% has only happened a handful of other times. That short history offers little indication of what to expect over the coming year. However, bull markets tend to last roughly five years, but this bull market is now just two years old which suggests cause for continued optimism. Solid earnings and a median gain during the first year of a presidential cycle of roughly 8% are also positive factors.

The S&P has been led by several mega-cap names that have performed particularly well. Thanks to solid returns for the eight biggest companies in the index, those eight stocks with market capitalizations in the trillions of dollars now account for 35.6% of the index versus a share of just 15.5% of the S&P for the top eight stocks a decade ago. The market has become more top-heavy and theoretically should be more volatile due to that concentration.

While all 11 S&P 500 sectors generated flat or positive returns last year, Technology and Consumer Discretionary are the only two sectors that have outperformed the S&P 500 over the last 20 years. This has left the index with concentrations in a handful of names in those sectors. The concentration of growth-oriented names in those sectors is one reason growth stocks outperformed value stocks again in 2024 (by about 19%), marking the seventh time in 10 years this has occurred. As the market broadens and other stocks gain strength, that could be supportive of returns more generally for 2025.

Venturing Beyond the Giants

Small- and mid-cap indices tend to have more value exposure which was part of the reason they lagged large-caps in 2024. Mid-cap stocks returned 13.9% for the year with small-caps trailing at +8.5% based on the return of the S&P 600. However, all the returns for small-cap stocks came in the second half of the year as it became increasingly clear the Federal Reserve would begin cutting interest rates. Lower domestic rates tend to favor small companies because they are more dependent on borrowing from banks versus larger companies that can access the capital markets. This has also pushed estimates for earnings growth within small-cap indices to high double digits for much of 2025.

Non-U.S. stocks had a tough year given the strength of the U.S. dollar. The dollar’s 7% appreciation during 2024 reduced the returns of foreign stocks by a commensurate amount, leaving developed international equity net returns at 3.8% and emerging market equity returns at 7.5% for the year.

Monetary Policy and Bonds

After aggressively increasing interest rates beginning in March 2022, the Federal Reserve reversed course and cut the overnight rate three times during 2024 by a total of 1%, leaving the Federal Funds rate at 4.25-4.50%. The Federal Open Market Committee suggested two more quarter-point cuts are expected for 2025.

With the yield on the 2-year U.S. Treasury roughly unchanged during the year at 4.22% and the 10-year yield up 0.66% to 4.53%, the yield curve normalized during 2024. Unlike the situation for the prior two years when the curve was inverted, this means that long-term rates are again higher than short-term rates. As a result, taxable and municipal bonds generated low-to-mid single-digit returns for the year. The high-yield market, which tends to move more in line with equities, produced some of the highest returns within fixed income with an 8.2% return for the U.S. Corporate High Yield index.

Alternative Assets

Based on the return for the S&P GSCI Gold Index, gold was up 26.6% during 2024 and outpaced even the above-average return of the S&P 500 thanks to its attractiveness in an environment with geopolitical uncertainty, lower interest rates, and the unease over U.S. debt levels having tripled since 2007. Meanwhile, the HFRX Index of hedge funds was up 4.8% for the year.

The Economic Backdrop

The strong stock market returns for the year occurred in an economic environment marked by solid GDP growth, modestly rising unemployment (up 0.5% year-over-year to 4.2% as of November 2024) and falling inflation. Despite the progress in slowing price increases, inflation remains above the Fed’s 2% target. The consensus for economic growth this year is for an expansion of roughly 2%. While this would be slower than 2024, the strength of the U.S. economy remains a tailwind for stocks.

What Lies Ahead for 2025?

One risk for 2025 could be the resurgence of inflation, particularly if wages increase strongly or if the effects of increased tariffs are passed on to consumers. Another risk could be a dampening of the euphoria over the prospects for artificial intelligence. Finally, valuation (as measured by the price/earnings ratio for the S&P 500) is about 30% higher than the 30-year average, though high valuations did not keep the stock market from achieving stellar returns in 2024. The environment is nonetheless changing and “what got you here might not get you there” as some say. Broadway Bank’s experienced, highly credentialed Wealth Management team continues to rigorously analyze each security that goes into client portfolios with a strong emphasis on risk management.

For questions or comments on any of the topics included in this newsletter, please contact Broadway Bank’s Wealth Management team at [email protected].